Muntanga Uranium Project

The Muntanga Uranium Project is Atomic Eagle’s flagship asset.

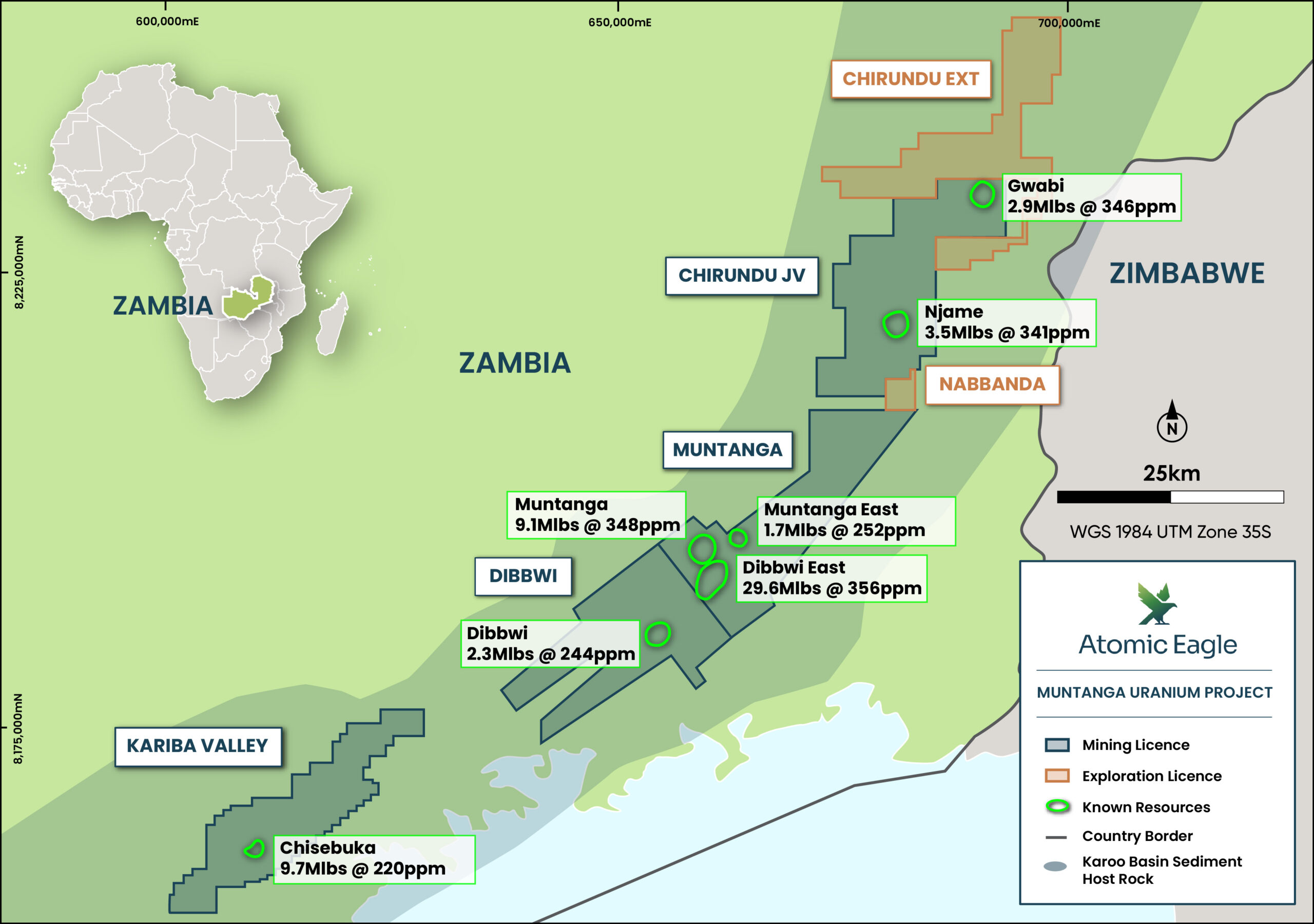

It is an advanced-stage development project located in the Siavonga and Chirundu Districts in the southeastern region of Zambia, within the highly prospective Karoo Supergroup.

The Project is 100% owned by Atomic Eagle, and it encompasses three mining licences – Muntanga, Dibbwi and Chirundu, covering 691 km2, that are located approximately 200 km south of Lusaka, north of Lake Kariba. Additionally, the Company holds two exploration licences for Nabbanda and Chirundu Extension, and a recently granted mining licence for Kariba Valley, which expands the total combined area to 1,100 km².

The project offers a rare combination of scale, resource definition, infrastructure access, and exploration upside.

Figure 1: Resource areas within the Muntanga Project License Area

Unlocking the Next Phase of Growth

Our long-term strategy is to expand our resource base and unlock the full potential of the Muntanga Uranium Project through systematic exploration and disciplined project development.

With extensive ground across Zambia’s highly prospective Karoo Basin, the company is focused on targeted growth, near-mine extensions, and new discovery opportunities across its portfolio.

Our strategy balances low-cost brownfield programs with progressive greenfield discovery work and new regional initiatives.

The objective is to grow the company’s mineral resource base, enhance project optionality, and ensure a steady pipeline of opportunities across multiple horizons, as below:

- Brownfield Opportunities – Immediate Impact

Atomic Eagle’s initial focus is on near-mine targets at Muntanga East and Chisebuka, where historical drilling has already identified strong uranium mineralisation. These programs aim to extend known deposits and add low-cost pounds rapidly through infill and step-out drilling. - Greenfield Expansion – Medium-Term Discovery

Exploration teams will advance the Muntanga North, Kariba Valley, and Dibbwi South areas, guided by detailed radiometric and structural mapping. These licences present significant scope for new discoveries within the same geological corridor as the main deposits. - Blue Sky Potential – Long-Term Growth

Beyond current licences, Atomic Eagle will assess additional prospective ground within Zambia’s uranium-bearing basins. This includes new tenement applications and potential partnerships with other holders of strategic ground.

Zambia: A Premier Destination for mineral resource development

Zambia stands out as one of Africa’s most stable, transparent, and resource-rich jurisdictions — an ideal home for the Muntanga Uranium Project. Since gaining independence in 1964, the country has maintained continuous democratic governance, underpinned by a strong legal framework based on English common law. This long-standing political stability and pro-mining government have fostered a secure and welcoming environment for international investment. Already the world’s 7th-largest copper producer, Zambia is rapidly expanding its mining horizons. The government has announced an ambitious plan to triple copper output to three million tonnes by 2031 while actively promoting the diversification of its minerals sector, including the development of uranium and other critical minerals vital to the global clean-energy transition.

Against this backdrop, the Project is well-positioned to benefit from the government’s diversification strategy and its commitment to the sector. The Project already holds the necessary mining licences and has filed the required studies to apply for Environmental Permits, which once secured will enable development to commence, subject to financing.

Finally, Zambia offers excellent access to both eastern and western markets through well-established export routes such as Walvis Bay in Namibia, enabling reliable supply to major nuclear markets in China, India, the United States, and Europe.

Project Highlights

- Shallow open pit mine and heap leaching with industry-standard, conventional downstream processing methods;

- Excellent local infrastructure with road access, water and grid power;

- Well-established export routes through Namibia, presenting the ability to supply Western and non-Western markets;

- No tailings dam required, reducing the environmental impact;

- Soft rock reduces powder factor and lowers mining costs;

Optimized ore processing:

- High liberation of minerals (only requires crushing to 25mm prior to agglomeration);

- LOM average recovery rates of at least 90% with rapid uranium recoveries within 21 days from start of heap irrigation;

- Low acid consumption, averaging less than 16.5 kg H₂SO₄ per tonne of ore treated, with Zambia’s position as a net surplus acid producer ensuring reliable local supply; and

- Quick start up: first uranium production expected within 4 months of mining.

Mineral Resource Estimate

SRK Consulting (Canada) (SRK Canada) prepared a mineral resource estimate (MRE) for the Muntanga Uranium Project in November 2017, in accordance with the Canadian Securities Administrators’ National Instrument 43-101 (NI 43-101). Following Atomic Eagle’s maiden drilling program for the Muntanga Uranium Project, the latest MRE was reported on 3 March 2026, including Chisebuka and Muntanga East.

The updated MRE is reported in accordance with the JORC Code and is summarised below.

| CATEGORY | U3O8 CUT-OFF [ppm] | DEPOSIT | TONNES [ppm] | U3O8 GRADE [ppm] | U3O8 METAL [Mlb] |

|---|---|---|---|---|---|

| Measured | 110 | Gwabi | 1.1 | 254 | 0.6 |

| 90 | Njame | 2.5 | 358 | 2.0 | |

| Indicated | 90 | Muntanga | 8.6 | 369 | 7.0 |

| 90 | Dibbwi | 3.2 | 253 | 1.8 | |

| 90 | Dibbwi East | 31.3 | 372 | 25.7 | |

| 110 | Gwabi | 2.7 | 374 | 2.2 | |

| 90 | Njame | 1.0 | 306 | 0.7 | |

| Total M&I | 50.4 | 359 | 40.0 | ||

| Inferred | 90 | Muntanga | 3.4 | 278 | 2.1 |

| 90 | Dibbwi | 1.0 | 213 | 0.5 | |

| 90 | Dibbwi East | 7.1 | 252 | 3.9 | |

| 110 | Gwabi | 0.2 | 272 | 0.1 | |

| 90 | Njame | 1.1 | 329 | 0.8 | |

| 90 | Chisebuka | 19.9 | 220 | 9.7 | |

| 90 | Muntaga East | 3.1 | 252 | 1.7 | |

| Total inferred | 35.8 | 238 | 18.8 | ||

| TOTAL | 86.2 | 309 | 58.8 |

Notes:

1. Mineral resources are constrained within an optimised pit shell using a uranium price of US$100/lb, mining costs of US$3.30/t, processing costs of US$9.00/t, additional mining costs of US$0.55/t, G&A costs of US$1.50/t, transport costs of US$1.50 and a royalty of 5%.

2. Mineral Resources are reported at a range of U3O8 ppm cut-off grades within the optimised pit shell.

3. Mineral Resources are inclusive of mineralisation in the low-grade U3O8 80 ppm halo but reported above the relevant cut-off and

classed as Inferred Resources. This mineralisation represents approximately 5 % of the total Mineral Resources metal (Mlb) for Dibbwi,

Dibbwi East, Muntanga. Njame and Gwabi. For Muntanga East and Chisebuka, a 90ppm grade cut off was used to define the

mineralisation.

4. Mineral Resources are not Ore Reserves and do not have demonstrated economic viability. There is no certainty that all or any part of

the Mineral Resources will be converted into Ore Reserves in the future.

5. All figures have been rounded to reflect the relative accuracy of the estimate.

Note: Mineral resources are not mineral reserves and do not have demonstrated economic viability. There is no guarantee that all or any part of the mineral resource will be converted into a mineral reserve. There is no direct link from an Inferred Mineral Resource to any category of Ore Reserves.

Muntanga Ore Reserve

The Muntanga Ore Reserve estimate was reported based on the guidelines of the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves, 2012 edition (JORC code) and the ASX Listing Rules. The Ore Reserve estimate is based on the 31 January 2024 Mineral Resource estimate for the Muntanga Uranium Project.

| Classification | Tonnes [Mt] | U3O8 Grade [ppm] | U3O8 Contained [Mlb] |

|---|---|---|---|

| Muntanga Pit | |||

| Proved | - | - | - |

| Probable | 8.4 | 331 | 6.1 |

| Subtotal | 8.4 | 331 | 6.1 |

| Dibbwi East pit | |||

| Proved | - | - | - |

| Probable | 31.2 | 317 | 21.8 |

| Subtotal | 31.2 | 317 | 21.8 |

| Total Project | |||

| Proved | - | - | - |

| Probable | 39.6 | 320 | 28.0 |

| Total Project | 39.6 | 320 | 28.0 |

Notes:

- All figures are rounded to reflect the relative accuracy of the estimate and have been used to derive sub-totals, totals and weighted averages. Such estimates inherently involve a degree of rounding and consequently introduce a margin of error. Where these occur, the CP does not consider them to be material.

- The Concession is wholly owned by, and exploration is operated by Atomic Eagle Limited

- The standard adopted in respect of the reporting of Ore Reserves for the Project, following the completion of required technical studies, is in accordance with the guidelines of the JORC code, 2012 edition, and have an Effective Date of January 1, 2025.

- The Open Pit Ore Reserves are reported with engineered pit designs using a cut-off grade per area varying between 70.1 ppm U3O8 and 85.1 ppm U3O8, which is based on a selling price of USD80 /lb U3O8, reference mining cost of USD 3.30 /t rock, additional ore mining cost of USD 0.55 /t ore, additional ore hauling cost of USD 0.18 /t ore-km, incremental depth mining cost of USD 0.05 /t/10m bench, processing cost of USD9.00 /t ore, royalty of 5 %, G&A of USD1.50 /t ore, port costs of 1.50 /lb U3O8 and recoveries varying per location between 74.6% and 93.3%.

- The Open Pit Ore Reserves are derived from a regularized block models of 5m x 5m x 2.5m (Muntanga) and 10m x 10m x 2.5m (Dibbwi East) and include an additional dilution and 5 % mining loss.

2025 Feasibility Study

In March 2026, Atomic Eagle released results of a Feasibility Study for the Muntanga Uranium Project, originally completed in March 2025, following completion of an independent engineering review.

Highlights

- Independent engineer PRODEO Consulting confirmed that the reporting production targets, capital costs and financial outcomes of the Feasibility Study are materially supported by reasonable technical inputs

- Atomic Eagle declared a maiden Probable Ore Reserve of 39.6 Mt @ 320ppm U3O8, containing 28 Mlb U3O8 in accordance with the JORC Code

- Key results from the Feasibility Study included:

- Production: Low-strip ratio open pit mine and heap leaching with industry-standard, conventional processing methods to produce an average of 2.2 Mlb U3O8 saleable product per annum.

- Optimised ore processing: Only requires crushing to 25mm for agglomeration.

- High process recoveries: Life of Mine (“LOM”) average recovery rate exceeds 90%.

- Low acid consumption: Average of approximately 20kg H2SO4 per tonne of ore treated.

- Long Project life: LOM of ~12 years.

- PRODEO and Atomic Eagle identified engineering optimisations to enhance the Feasibility Study however, increasing the uranium resources is the precursor to achieve a step-change in production scale.

- Resource growth will underpin an increased production throughput to significantly enhance the Project’s economic outcomes.

| Item | Units | Value |

|---|---|---|

| Production and Mining | ||

| Mine life | Years | ~12 |

| Ore Mined | Mt | 39.6 |

| Ore Grade | ppm U3O8 | 320 |

| Plant throughput | Mtpa | 3.5 |

| LOM production | Mlb U3O8 | 25.3 |

| Average annual production | Mlb pa | 2.2 |

| Financial Parameters | ||

| Pre-production capital costs | US$ million | 282 |

| Operating costs (C1) | US$/lb | 32.20 |

| Post-tax NPV8 | US$ million | 243 |

| Post-tax IRR | % | 20.8 |

| Payback period | Years | 3.5 |

| LOM Free Cash Flow | US$ million | 672 |